Is EBITDA a Measure of a Company’s Financial Stability, or a False Prophet?

Why Cash Flow from Operations Provides Better Support for Trade Credit Decisions

Decisions to extend trade credit are based on an assessment of a company’s financial stability, competitiveness, and desire and ability to pay to the seller’s terms. Many of these decisions are made based on factors other than what is revealed in a potential customer’s financial statements. However, based on a seller’s credit policy, a thorough review of financial statements is a required gate an applicant has to pass through before any credit line is approved.

There are many ratios and indicators on which credit decisions can hinge. The key is to focus on areas that truly reveal a company’s obligations and the applicant’s ability to generate the cash to pay them. This requires a clear-eyed look at the factors that actually drive a company’s cash flow, the lifeblood of any company. It is cash flow that supports a company’s ability to sustain and grow operations and meet its obligations.

EBITDA is an Indicator of Company Health

If an analyst depends on an EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) calculation to calibrate a company’s health, it is important to realize it is an indicator but not a statement of the actual cash generated to meet obligations. EBITDA does not illustrate cash flow. It does provide a clearer picture of a company's operational performance by stripping out the effects of financing and accounting decisions, making it a popular metric for comparing profitability across businesses and industries.

In the EBITDA calculation, "Earnings" refers to a company's net operating income before deducting certain expenses. Put another way, it represents the Operating Profit generated from the core business operations, including depreciation and amortization, but excludes the costs of financing (interest), taxes on earnings, and non-cash expenses like depreciation and amortization. Operating profit considers Gross Operating Income, the total revenue generated from operations, such as rental income in real estate or sales revenue in a business, less Operating Expenses, and the expenses required to run the property or business, excluding interest, taxes, depreciation, and amortization.

Operating Profit is calculated as total revenue minus the cost of goods sold (COGS) and all operating expenses (e.g., selling, general, and administrative expenses, SG&A). It includes all operating costs of a business, including those not directly tied to property or asset-specific operations.

Calculating EBITDA

Start by referring to a company's annual report, SEC Form 10-K, or quarterly 10-Q report filed with the U.S. Securities and Exchange Commission. Go to the operating statement, and you will find line items for all of the items in EBITDA. Add the expenses and subtract any income (such as interest income), then add the total to the reported net income or net loss.

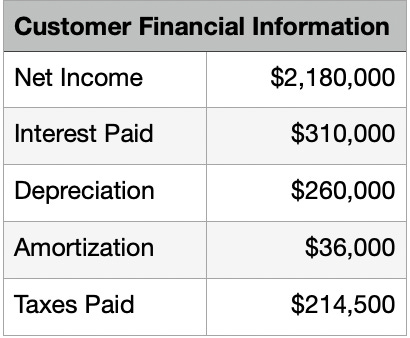

Let’s look at the following example:

EBITDA = Net income + Taxes + Depreciation + Amortization + Interest

Based on the information provided above:

$2,180,000 + 310,000 + 260,000 + 36,000+ 214,000 = an EBITDA of $3,000,000

Calculating the EBITA Margin

Another way to use EBITDA is to calculate the EBITDA margin by dividing EBITDA by total revenue. This illustrates how operating expenses are affecting the customer’s gross profit. The higher the EBITDA margin, the less financial credit risk.

Using our example, your customer has an EBITDA of $3,000,000 along with a total revenue of $30,000,000.

EBITDA margin = EBITDA / Total revenue

$300,000,000 ÷ $30,000,000 = 10% EBITDA Margin

This point of comparison will vary depending on the industry, type of company, and macroeconomic factors.

Beware! EBITDA is an accounting calculation. Trade credit is based on the working capital and cash flow needed to meet obligations. EBITDA can easily be used to hide financial facts. It can be misused to make a company's earnings appear greater than they really are by obscuring warning signs, such as high levels of debt, escalating expenses, or lack of profitability.

However, when comparing the profitability of one customer to another, EBITDA can be of some help. If a customer’s EBITDA is negative, it is an indicator of poor cash flow. With that said, a positive EBITDA doesn't necessarily mean the customer is highly profitable.

Critical Factors to Consider

Be sure you are comparing companies with an analysis that is both current and audited.

Understand how EBITDA has been calculated and any adjustments included in the calculation.

Dive deep enough into the facts to make sure you have all of that information before making any conclusions.

For newer companies, EBITDA may exclude start-up expenses.

EBITDA does not account for changes in working capital. A company's liquidity fluctuates along with interest, taxes, and capital expenditures, which are actual expenses that businesses must account for. In contrast, a company may have low liquidity if its assets are difficult to convert into cash but maintain a high level of profitability.

EBITDA can also provide a distorted picture of how much money a company has available to pay off interest. When you add back depreciation and amortization, a company's earnings can appear greater than they really are.

EBITDA can also be manipulated by changing depreciation schedules to inflate a company's profit projections.

EBITDA does not directly reflect the actual cash available from accounts receivable or other cash sources.

Although EBITDA is often used to estimate operating profitability and is sometimes seen as a proxy for cash flow, it does not represent the real cash inflows or outflows within a company. EBITDA excludes non-cash expenses like depreciation and amortization, making it a useful metric for understanding operational profitability. However, because it doesn't consider changes in accounts receivable or other working capital accounts, it can’t show the actual cash collected.

Changes in accounts receivable are part of a company’s working capital adjustments and affect cash flow. If a company has made sales on credit, those sales increase revenue (and EBITDA), but the cash from accounts receivable hasn’t been collected yet. EBITDA does not account for cash that has or hasn’t been collected. It also ignores cash outflows for interest, taxes, and capital expenditures. As a result, it can overstate the cash available to a company.

A Better Cash Flow Measure

A more accurate measure of actual cash flow is Cash Flow from Operations (CFO) This metric is found on the cash flow statement. The CFO calculation adjusts for working capital changes, including accounts receivable, inventory, and accounts payable. It reflects the actual cash collected and spent in operations.

The Value of Tracking CFO Trends: Analyzing a company’s CFO trends over several recent reporting periods will provide an Analyst with a clear view of the cash a business generates (or uses) through its core operations over time. This also provides a view independent of financing and investing activities. Monitoring these trends provides revealing operational efficiency insights of value to trade creditors.

CFO is a More Revealing Performance Indicator: Tracking CFO trends will offer valuable insights into a company’s operational efficiency, sustainability, liquidity, and overall financial health. This will help you make more informed decisions. CFO shows the actual cash generated by the business's primary activities. This is more revealing than net income, which can be affected by non-cash items (like depreciation) and accounting adjustments. CFO trends highlight whether the business is consistently generating cash from its operations, offering a true picture of financial health.

Five Specific Benefits CFO Provides to Trade Creditors Decision Process:

Sustainability and Profitability: Positive and growing CFO trends suggest that a company’s operating activities are sustainable and can cover expenses, reinvestments, and possibly dividends. A declining or negative CFO over time may indicate operational inefficiencies or potential liquidity issues, even if accounting profits look healthy.

Working Capital Management: CFO reflects changes in working capital items like accounts receivable, inventory, and accounts payable. Tracking trends in CFO can reveal how efficiently a company is managing these areas. For example, an increasing CFO might indicate improved cash collection or inventory management, while a declining CFO might suggest challenges in these areas.

Funding for Growth and Obligations: A strong CFO trend suggests that a company has the cash flow necessary to fund growth, capital expenditures, debt payments, and other obligations without relying on external financing. Conversely, declining CFO trends could signal reliance on debt or equity financing, which could pose risks if sustained.

Investor Confidence: Consistent, positive CFO trends provide investors with confidence that the company is financially stable and capable of generating sufficient cash to support its operations, growth, and returns. Investors often look for companies with strong, stable cash flows, especially during economic uncertainty or industry downturns.

Early Warning of Financial Issues: CFO trends can serve as an early warning system. For example, if net income is rising but CFO is flat or declining, it may indicate that revenue is not being effectively converted into cash, which could point to potential issues like rising accounts receivable or inventory problems.

The Bottom Line

While EBITDA provides valuable insight into a company's operational profitability, you should use it as a measure of financial stability for making credit decisions with some caution. EBITDA can overstate cash availability by excluding essential cash-related factors like working capital changes, interest, and taxes.

Cash Flow from Operations (CFO) offers a more accurate and comprehensive view of true financial health for trade creditors seeking a reliable indicator of a company's capacity to meet obligations. Tracking CFO trends allows for better-informed credit decisions. It reflects a company’s actual cash generation from core operations over time.

CFO provides key insights into working capital efficiency, sustainability, funding capacity, and potential risks, positioning it as an indispensable measure in the credit assessment process. Consequently, while EBITDA can be a helpful tool for comparing operational performance, the CFO stands out as the more reliable indicator of a company’s ability to support operations, fulfill obligations, and sustain long-term growth.